Developer-Led Landscape: 2021 Edition

$49B in annualized recurring revenue, up 22% from 2020, from over 1000 companies whose products were sold or influenced by developers!

Starting in 2009, I began tracking each company whose products were sold to, purchase-influenced by, or consumed by software developers.

I call this the Developer-Led Landscape and published the first version in September 2020.

The landscape was warmly received and is one of the more definitive and comprehensive papers covering the companies and products that are developer-oriented.

We’ve updated the landscape with activities observed over the past year and from the 500 engagements we have had with entrepreneurs, investors, and technologists.

Previous Developer-Led Landscape Papers

Developer-Led Landscape: Latency-Optimized Development

Developer-Led Landscape: 2021 Trends Foretell New Approaches To DevOps

Developer-Led Landscape: Cloud-Native Development

Developer-Led Landscape: The Original

The Landscape — By Category, Segment, ARR, and Growth

The database of companies mapped to category, segment and specialization are kept in a public Google sheet. The methodology for how we determine which segments are included or excluded along with major definitions are included in a GitHub repository.

There are now 1004 companies publishing 1286 product lines that generate $49,002M in ARR.

The growth rates highlighted in green are segments whose rate of growth increased over the previous year.

The largest category is Development Platforms with 420 companies publishing 496 products that generate $32,706M ARR. This is followed by Development Infrastructure with 352 companies publishing 461 products generating $8,712M ARR and Software Delivery Lifecycle with 118 companies publishing 135 products generating $4,275M ARR. And finally, in the “we like the struggle” category, Developer Tooling has more companies generating less ARR with 165 companies publishing 194 products that produce $3,329M ARR.

Developers Are The Engine Behind Digital Transformation — Dev Landscape Grew $9B ARR, 22% YOY Growth, Faster GROWTH Than Any Time In The Previous Decade!

Across all of the companies that we tracked, ARR increased $9B year over year, which is a 22% growth rate. While we have only been publishing this landscape since 2020, the tracking of companies through the previous decade were generally growing 15% collectively, weighed down by large legacy products that had flat growth offset by innovators in new categories.

Accelerating growth, a situation where a well established segment grows at a faster percentage in subsequent years, is extremely rare.

The acceleration in this market is a reflection on the importance of digital transformation for all businesses, the relative acceleration in priorities that companies are placing upon digital transformation, and a recognition that developers are the engine that is driving digital transformation.

We Discovered 224 New For-Profit Product Lines Launched

With most companies, if they have a dominant product that covers a single segment, we lump all of their revenues and mini-products into that single offering. But, as companies grow, they launch products that have unique brands that target new segments. We add these entries to the landscape and recognize each product as separate entries.

The 1004 companies in the landscape have published 1263 product lines.

Digital Transformation Acceleration Has Caused New Segments To Emerge As Growth Leaders

There has been a significant shift in the segments which are showing growth leadership from one year to the next.

It is not a surprise that API as a Product has become the fastest growing segment across the developer ecosystem. APIs drive broader forms of adoption and are conducive to a consumptive business model. In an era where most human interaction is moving towards a digital form, APIs that reinvent classic businesses are gaining traction and taking share from legacy businesses.

What is a little unusual is the emergence of classic segments which are nearly 40 years old emerging as growth leaders across the entire spectrum of developer technologies.

Version Control, SRE + Debugging, and CI + CD + Build have leapt into the top growth segments after having moderate growth in 2020. The driver is the broader focus on digital transformation - many more funded projects launched or growing - requiring broader consumption of foundational products around the construction of software.

New Developer Companies Were Launched 2.75x Faster Than They Were Shuttered / Acquired Over The Past Year

In the past year, we came across 117 new for profit companies that have products in this landscape. We are sure that this number is under represented as there are probably dozens, maybe even 100s, of self service offerings being published on Product Hunt created by small teams, which are likely relevant but also appearing so rapidly that proper engagement, analysis and activity following is difficult.

Across the landscape, there were 42 acquisitions / shutterings from companies listed in last year’s landscape. The acquisitions represent $565M in last year’s ARR, indicating that large platforms were buying quality and market leadership. Most of the shutterings that we came across were acqui-hires with only a single known bankruptcy. There could be many more bankruptcies that have eluded our filters.

Interestingly, with so many new companies launching faster than the rate of acquisition, the average age of companies in the developer landscape has decreased from 15.8 years in 2020 to 14.5 years in 2021.

Dominant Companies Still Dominate … Mostly

We commented last year that there is a tendency that when a new category in the developer landscape emerges, the top 2-3 companies will grab the majority of the market.

For the most part, there is little shift in the allocation of revenue to the top companies in each segment.

The most notable exception is in the Test Automation market. It’s already crowded with many new entrants and a plethora of competitors that generate north of $5M in total ARR. In the past year, those new entrants gained more share than their larger, usually legacy-oriented counterparts. The top three companies now only control 25% of the market vs. 43% last year.

117 Companies Added To The Landscape Have Raised A WHOPPING $1B

It’s an amazing time to be an entrepreneur.

Early capital is cheap and accessible, and the barriers to creating new tooling are low for developers, especially when they have deep domain understanding (i.e., building tools you’d use as a developer for other developers).

Of the 117 new companies we identified over the past year, they raised an average of $8.85M each from VCs. This is remarkable, as the average seed stage investment hovered around $3M through most of the past decade. While some of these companies existed for a couple years (and we just discovered them recently), many of these companies were able to raise multiple rounds of venture capital within the same year. We see this as a reflection of hungry investor appetite in innovative approaches to DevOps and also a reflection of the faster velocity witnessed by many of these companies which employ Product-Led Growth (PLG) styles that emphasize developer discovery and activation over sales-led motions.

Note - some of these companies existed last year, but well, we didn’t know about them and so they weren’t included last year. They are here now, and still treated as a company that is new to the landscape.

Liquidity For Value Creation Runs Thin - 22 Acquisitions and 4 IPOs Delivers Less Than $35B In Transactional Value

Given the pace of investing and the size of the landscape with over 1000 companies, only 25 companies had defined transactions that offered investors, founders, and employees an opportunity at liquidity.

Most of the liquidity was generated through 4 tremendous IPOs with Confluent taking the lion’s share of the value. JFrog was a Dell Tech Capital portfolio company, so congrats one last time Shlomi and team!

There were 22 acquisitions across the Developer Landscape.

As in any year, there are a couple of anchor acquisitions that fundamentally shift the competitive dynamics. This includes Episerver’s acquisition of experimentation vendor Optimizely, ServiceNow’s acquisition of observability vendor Lightstep, CollabNet merging into Digital.ai and follow through acquisition of XebiaLabs, and Twilio’s monster acquisition of Segment for $3.2B.

Private Developer Landscape Companies Raised a RIDICULOUS $16B in Venture Capital This Year Almost Doubling All Previous Private Company Raises!

Venture capital has never been easier to obtain, whether a developer startup or a growth company.

In 2020, private companies had collectively raised just over $21B cumulatively. This year, those same companies have raised $37B, a net increase of $16B! If you net out the impact of IPOs, the impact is even more significant.

Given that most financing rounds will work to obtain 10-20% equity ownership in a company during the round, a back of the hand assessment indicates that the private, VC-funded companies that raised in the past year were collectively valued at up to $160B during their latest financing.

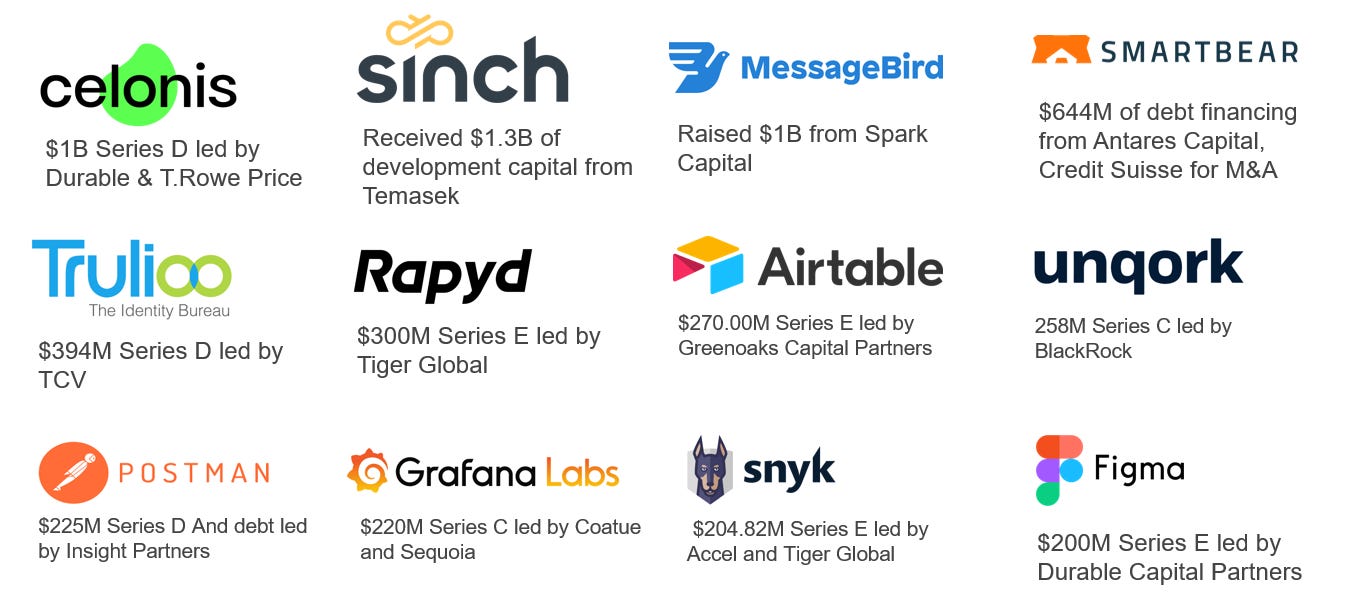

Mega Rounds Are Going Mega Mega - Make Way 10 Figure Funding Rounds

Being a unicorn where your market cap is valued at a billion dollars is so blase. The new bar is to raise unicorn money, by having a round of at least $1B in new funding.

Three of the companies in the landscape raised rounds that were over $1B. Further, there are 85 companies in the landscape that have raised collectively more than $250M.

and I guess only raising $100M makes you so-so?

Much of this venture capital signals the emergence of the developer as the engine behind Product-Led Growth companies. Traction and accelerating activation driven by the nearly 100M global developers reflects future value that venture capitalists are willing to aggressively buy into. Developers are shining a light on how to undermine inflating sales & marketing spend — more on that trend below.

Dell Technologies Capital Continues To Invest in Developer Landscape Early Stage Innovators

Dell Tech Capital was particularly excited to participate in this wave with our lead financing in Developer Landscape companies Bodo.ai (making NumPy Python so fast that you don’t need Databricks), Archipelo (stealth), and Fly.io (a new kind of PaaS that moves applications and databases to be closer to end users).

This continues our decade’s long commitment to DevOps investing, following our investments in JFrog (the leader in artifact repos), Redis (caching at its best), MongoDB (did you see their stunning quarterly results shooting their stock up 25% in a day?), Bastion Zero (simple secure server access for devs), Treeverse (version control for data lakes), Lightbend (makers of Akka distributed dev platform), MinIO (640M downloads of their S3-like object store), NS1 (trillions of transactions for API-driven DNS), OpsMx (continuous verification and delivery). And I have personally been active in this arena with investments in WSO2, Sauce Labs, InfoQ, Codenvy, Roguewave, and Sourcegraph.

Analysis: $16B Flows Into Private Companies While $35B Flows Out; Soft IPO Market; Limited Late Stage Appetite; Beware Liquidity Traps, Consolidation.

I am startled by these results, and you should be too.

More money flowed out of DevOps companies than flowed into it during the past year. This is a net positive, right?

With the market for developers the hottest it’s ever been, the pace of money flowing out of investments should be significantly higher than the money flowing in.

Liquidity should be at all time highs for companies in the dev landscape.

If developers are strategic, then strategic vendors should be acquiring at rates that outpace investor enthusiasm, perhaps as high as 5:1. Should we be seeing $80B in exits, instead of $35B?

IPOs Were Underwhelming

Most of the $35B were across only 4 IPOs, which have lockups and requirements for founders / owners / officers to limit their liquidity.

Axios reports that we’ll get close to 375 IPOs in 2021 after only 218 in 2020, and that doesn’t include nearly 500 SPAC IPOs or direct listings. With almost 900 companies getting liquidity, and few of those coming from the DevOps arena, the underlying dynamics are concerning.

The bar for DevOps IPOs has leapt. The previous threshold was typically $100M ARR and it’s now closer to $200M with a sustainable >40% growth profile. In other words, the public markets only want to absorb DevOps companies that are playing in multi-billion dollar markets, or have the potential to expand into markets that are collectively $10B in size.

So, developers are strategic to the markets, only as long as they are coupled to a mega market with abnormally large budgets.

Late Stage Acquisitions Were Timid

The late stage acquisition market was timid in the past year. Other than Twilio’s $3.2B acquisition of Segment, large scale developer acquisitions were relegated to Private Equity, and most of those were under $1B in total value. So it seems that strategic money also is not pouring in to acquire companies.

Developers Not Strategic or Valuations Out of Control?

What does it mean for the companies that are capable of $20-$200 in ARR and growing slowly? That should be good value for an acquirer that places an emphasis on building access to developers. But no one is buying? Why?

Either the revenue isn’t strategic, they don’t actually value developers the way that many companies claim to, or valuations have gotten unrealistic.

Valuations are trading as high as 100x revenues for early stage developer companies. So for a strategic to step in and acquire something, either:

that company must be mega strategic (i.e., a true once-in-a-generation opportunity), or

do an acquihire where the business has no further ability to continue fund raising, or

buy nothing.

With so few mega acquisitions happening, we can start to see evidence that there aren’t that many companies in the landscape that are deemed mega strategic. The lack of acquisition activity is a reflection of buyers not able to find a value alignment with sellers. In other words, there is a value mismatch.

So now we have a modern crop of aggressive investors who are bidding developer landscape companies with $5-$40M ARR into the valuation stratosphere on the expectations of continued, significant growth.

Only the companies that are true platforms have the potential for an IPO, such as a Gitlab or Cloudbees, but that bar is so high as they’ll have to burn an uncomfortably large amount of cash in order to sustain the 50% growth that public market investors crave. A few select companies will have break away speed, but the rest will be faced with a financial identity crisis - lower growth, a tightened fund raising environment, and being forced to right-size operating expenses to the nature of their business.

Are Developer Businesses Turning Into Liquidity Traps?

Could these investments turn into liquidity traps for their investors?

With the IPO viability threshold increasing to be reachable by a smaller crop of companies, a growing basket of developer landscape companies that generate $10-$100M in revenue with <40%, and a shrinking appetite of strategic acquirers, what happens to all of these companies that have collectively raised >$100M from Venture Capitalists?!?

Are There Pockets Of Opportunity In The Developer Landscape?

Heck yeah, and Dell Technologies Capital will continue to be aggressive in this market. The nature of the opportunity has shifted. Fundamental disruptions, paradigm shifts, autonomous development, security, and self-growing communities all have the hallmarks necessary to deliver outsized value in this large and diverse market.

Analysis: Power Shift From CIOs to Developers; Developers Engine Behind Digital Innovation; Developer Empowerment Drives PLG Business Growth; Tail End of 15 Year Fragmentation Wave

While these thoughts are my own and in my own words, I have been influenced by many great leaders and thinkers in this space, and so their own perspectives are indelibly linked and somehow part of this as well.

Any Developer With An Idea

Developers have blossomed from idiosyncratic isolates to innovation engine driving digital transformation. Any developer with an idea has been empowered to execute their ideas. Cheap fractional cloud services purchased with a credit card, the proliferation of free and accessible open source tools, a global (huge) community of collaborative peers, and one click product distribution through the Web, URLs, or APIs make the barriers to executing an idea small, and shrinking. Atlassian is the strongest representation of this trend.

Power Shift From CIOs to Developers — Innovation Is Democratized

Developers are able to leave environments where their personal choice over tools and platforms are not honored. The willingness of competitors to prioritize developer choice and the empowerment of developers who can implement their own ideas have eroded the power of the CIO as decision maker.

Dev Empowerment Drives Emergence of Product-Led Growth Companies

Costly sales & marketing spend has become a developer’s opportunity.

Developers do not suffer fools and will only pay for value. With developer empowerment and their ability to make purchasing decisions in greater quantities, businesses must cater to the proclivities and attitudes that the developer class embody.

This includes a developer’s willingness to bypass companies where an immediate self-trial and usage pattern is not available. Developers who are forced to work with sales teams in companies that embody a Sales-Led Growth motion are more likely to skip engaging with the company or make a negative recommendation.

This has made open source activity, Web site engagement, and mobile installs a quantifiable measure of how a business is doing and their rapid growth is a success predictor.

PLG companies are capturing more venture capital, grabbing larger venture rounds, and obtaining high valuations as these businesses are upending industries where sales & marketing operating costs are substantially higher. These companies embody a self-discovery, activation, consumption, and expansion model for GTM. Think about Twilio, MinIO, Snyk, and Vercel as representative examples.

Over 50 Years The Developer Landscape Goes Through 15 Year Fragmentation / Consolidation Cycles Driven By The 3 Waves Of Software Supply Chain Industrialization

Finally, DevOps seems to go through 15 year mega waves of fragmentation and consolidation triggered by paradigm shifts in software construction behaviors. The last transition was in 2005 with the introduction of git which launched a massive fragmentation and disruption to the platform vendors which were IBM and Microsoft.

We are now witnessing the beginning of a mass consolidation emerging around mega platforms - GitHub, Gitlab, Snyk, JFrog, and Datadog. Each of these vendors have aggressively been launching projects that are adjacent to their core proposition, making acquisitions, and spinning a vision of delivering DevOps services across the developer spectrum.

These mega waves of fragmentation and consolidation are catalyzed by industrialization shifts. We’ve gone from manual, waterfall construction of complex software systems, and as our understanding of the software supply chain improves, we are increasingly able to abstract and automate it.

All of this is the pretense to our future, where software development is autonomous.

Onward!